The Hidden Mathematics of Modern Debt

Lenders prefer to present your loan as a neat, easily digestible monthly number that fits cleanly into a household spreadsheet. However, the mathematics operating under the hood of a modern mortgage, commercial loan, or student financing agreement are rarely that straightforward. A basic calculation almost never reflects the actual interest burden you carry over a decade or two, especially once you introduce staggered builder payouts, shifting macroeconomic rates, or negotiated grace periods.

Taking on long-term debt is one of the most consequential financial choices a person makes. Whether you are funding a custom build, purchasing retail space, or financing an advanced degree, understanding the granular cost of borrowing is essential to maintaining stability and bypassing wealth-draining structures.

That is exactly why we built this advanced loan EMI calculator. We designed it specifically to handle the messy, variable real-world factors that standard calculators gloss over. The objective is simply to provide everyday borrowers with the same algorithmic forecasting used by the bankers sitting across the negotiating table.

By inputting your base loan parameters, this tool instantly breaks down what fraction of your payment actually reduces your debt versus what is lost to interest overhead. Crucially, if you are managing a complex transaction, the advanced panel allows you to map out staged disbursements across years, adjust compounding frequencies, and project multi-year floating rate hikes to visualize your exact exposure.

What Triggers an Advanced EMI Setup?

An Equated Monthly Installment (EMI) represents the fixed payment a borrower makes on a specific calendar date. EMIs are designed to systematically clear both the generated interest and the remaining principal over a set timeframe, aiming for a zero balance by maturity.

A basic calculator operates in a static vacuum. It assumes the loan is handed over as a single lump sum on day one, and assumes the central bank will never touch interest rates for twenty years. Real life rarely works this way. An advanced tool mirrors dynamic banking practices. It seamlessly adapts to mid-tenure rate hikes, delayed payouts, or student grace periods without fracturing the underlying math.

By offering the ability to manipulate specialized features like moratoriums (and forcing you to clarify whether that interest is paid out-of-pocket or capitalized into your principal), this repayment schedule calculator acts as a financial sandbox. It allows you to model economic stress cases and test how resilient your finances are to rate jumps before signing binding contracts.

Understanding the Amortization Curve

To navigate debt effectively, you must understand amortization. This is the mathematical process of distributing a loan into a series of fixed payments over a timeline. While the EMI leaving your bank account remains identical every month, the internal ratio of what that money actually pays for shifts entirely over the loan’s lifespan.

Banks aggressively front-load interest. During the initial years of a 20-year mortgage, a high percentage of your monthly EMI is devoted solely to satisfying the interest generated by the large outstanding principal. Only a fraction genuinely reduces the core debt. This structural reality is why borrowers are frequently surprised to look at their balance after 60 months of payments, only to find the debt hasn’t decreased materially.

An advanced EMI calculator with an amortization schedule exposes this shifting curve. By examining the generated table, you can pinpoint the exact month where your EMI finally begins paying down more principal than interest. Understanding this pivot point is critical for making strategic refinancing moves; if you attempt to close a loan too late into its schedule, you have already paid the bank the vast majority of their expected profit.

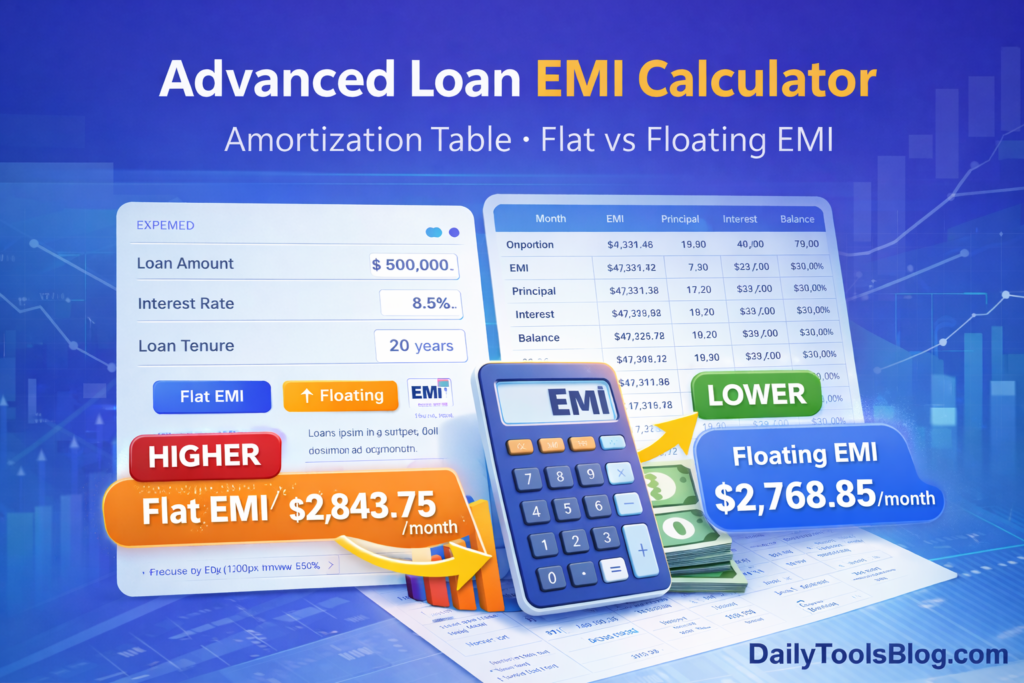

Core Math Engine: Flat vs. Reducing Balance

The calculation engine adapts entirely based on the method you select, tracking exactly how the bank views your remaining liability.

The Reducing Balance Architecture

For standard residential mortgages, personal loans from recognized banks, and modern vehicle financing, the system natively utilizes the reducing balance method. Here, the active interest component shrinks month by month, because the new interest charge is computed strictly on the principal balance that remains unpaid.

The Flat Rate Trap

If you select the flat rate mode—a structure sometimes used by micro-lenders or localized financiers—the tool stops using the reducing curve. Instead, the total lifetime interest is calculated upfront on the original loan amount for the entire tenure. That total interest burden is added to the principal, and the combined sum is divided equally across the months. This makes an 8.5% flat rate vastly more expensive than an 8.5% reducing rate.

Detailed Tutorial: Modeling Complex Loan Scenarios

To demonstrate the specialized mechanics of this advanced tool, let’s walk through a complex, realistic borrowing scenario using the interface above. We are modeling a situation that includes delayed property payouts, a construction grace period, and macroeconomic rate changes over a sub-decade timeline.

Phase 1: Setting the Baseline

The foundation of any calculation begins with the primary metrics. In this example, we are analyzing funding for an under-construction property requiring tranche disbursements.

Initial Inputs:

- Loan Amount: ₹42,50,000

- Annual Interest Rate: 9.15%

- Loan Tenure: 8.5 Years (102 Months)

A basic calculator would immediately spit out a standard EMI based on these three numbers. However, to handle tranche payments, we must click the “Advanced” toggle to unlock the simulation modules.

Phase 2: Defining the Financial Structure

Once inside the Advanced panel, the first modules dictate how the algorithm accrues interest.

EMI Calculation Type: For reputable property loans, select Reducing Balance EMI. This ensures that every time a payment clears, the active interest for the following month is calculated on a smaller base.

Interest Calculation & Compounding Frequency: You must dictate how the lender compounds generated interest. We set the Interest Type to Compound Interest and the Frequency to Yearly. This means the bank takes a snapshot of accrued interest every twelve months and recalculates the burden. Setting this to Monthly compounding would tangibly increase the total interest paid.

Phase 3: Managing Disbursement Stages

If you are building a property, the bank will not deposit the entire ₹42,50,000 upfront. They disburse funds in restricted tranches as construction milestones are met. Crucially, you should not pay interest on money the bank has not yet released.

Opening the “Loan Disbursement Stages” section, we deliberately break our core amount into distinct lifecycle payouts:

- Stage 1 Amount: ₹21,25,000 disbursed initially on a specific date.

- Stage 2 Amount: the remaining ₹21,25,000 disbursed exactly 14 months later.

By inputting specific dates, the calculation engine delays the principal liability for the second half of the loan, mathematically lowering the interest burden during the initial construction phase.

Phase 4: Configuring the Moratorium (Grace) Period

A moratorium is a formally designated period during which the borrower is not required to make standard EMI payments—common in education loans or construction mortgages. However, pausing payments does not pause the interest meter.

Example Configuration:

- Enable Moratorium Period: ON

- Duration: 18 Months

- Interest During Moratorium is set to Compound.

- Capitalise Interest After Moratorium?: Yes (Add to Principal).

- Moratorium Treatment: Include in Tenure.

Because we chose to Capitalize the Interest, the interest generated during that 18-month grace period is permanently added directly into our core principal liability. When active repayment starts, the new principal will be larger than the initial ₹42,50,000 sum.

Furthermore, because we selected “Include in Tenure,” the overall total life cycle of the loan has not been extended. The bank is forcing you to pay off a larger capitalized principal in a shorter active period, which leads directly to a noticeable spike in the required monthly EMI.

Phase 5: Plotting the Floating Rate Timeline

Very few long-term loans remain secured at their introductory rate. Central banking policies shift, dragging retail lending rates up and down. An advanced projection must account for these shocks.

We toggle the “Enable Floating Rate” switch to ON to plot an escalating timeline:

- Rate Hike 1: New Rate of 9.35%, Effective at Month 15.

- Rate Hike 2: New Rate of 9.50%, Effective at Month 28.

- Rate Hike 3: New Rate of 9.85%, Effective at Month 42.

By defining the exact “Effective Month”, the algorithmic engine knows when to halt the baseline calculation, inject the new interest rate onto the remaining unpaid principal at that exact moment, and recalculate the required EMI for the rest of the tenure.

Interpreting the Output and Internal Rate of Return (IRR)

With our structure finalized—staged payouts, a capitalized 18-month moratorium, and escalating floating rate hikes—we hit the “Calculate EMI” button. The resulting dashboard highlights the ultimate trajectory of the loan.

The dashboard presents a finalized Monthly EMI, Total Payment, Total Interest, and the Principal After Mora. This last metric is the smoking gun of the moratorium period trap: even though we only legally borrowed ₹42,50,000, the bank added the unpaid interest to our permanent debt load before we made an actual payment.

More importantly, the dashboard calculates the true Effective ROI (IRR). Even though our nominal rate started at 9.15% and floated up to 9.85%, the Internal Rate of Return dynamically calculates the timeline of your cash outflows against staggered inflows. Because the bank delayed giving us the second payout by over a year but capitalized compound interest on the first tranche anyway, the true annualized cost to your wallet over the entire lifecycle is mathematically proven to be higher than the nominal rate suggests.

Frequently Asked Questions

What is the difference between a Flat and Reducing balance?

A flat rate calculates your expected interest entirely on your original principal for the full tenure, completely ignoring your ongoing payments. A reducing balance calculates interest only on the unpaid principal left over each month, dropping your interest burden dynamically.

Does this advanced tool support exact compound interest tracking?

Yes. By utilizing the Advanced tab, you can switch the Interest Calculation block to compound and pick your preferred tracking frequency, ranging from daily compounding to yearly compounding.

Can I customize a moratorium grace period for an education loan?

Absolutely, you can toggle the Moratorium Period setting, input your required delay in months, and instruct the tool whether the accrued interest should be paid simply out-of-pocket or capitalized straight back into the principal amount.

How exactly does the algorithmic engine calculate the Effective ROI?

The backend system utilizes the Internal Rate of Return (IRR) algorithm across all dynamically generated cash flows. This ensures that the time value of money, which is distorted by staggered disbursements and shifting mid-term rates, is accounted for accurately.

Can I project future interest rate changes?

Yes, you can easily add multiple projected rate hikes mapped to specific future dates by enabling the Floating Rate of Interest toggle, allowing you to stress-test your monthly household budget against shifting economic scenarios.

Is the generated amortization schedule printable or exportable?

There is a securely integrated download button that cleanly exports the entire calculation table into a standard CSV file meant for deep offline accounting or spreadsheet analysis.

Why is the floating rate option disabled when I select flat rate?

If you affirmatively selected “Flat” EMI calculation mode, the integrated tool safely disables the active floating toggle to prevent calculation errors. Flat rate loans strictly lock in a fixed interest burden upfront based purely on the original borrowed sum, so mid-tenure variable rates do not mathematically apply.

Comment Guidelines